Analysis Of 11 U.S. Ad Revisions Shows Some Planetoids Aligning

Eleven Revisions Later, Planetoids Align

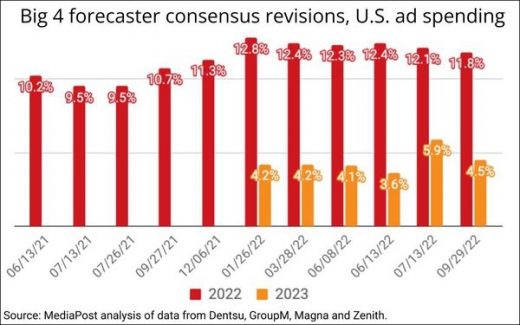

After 11 revisions by the Big 4 agency forecasting units, the consensus for this year’s U.S. ad growth estimates has been remarkably stable, despite an array of disruptive macroeconomic events.

And while Thursday’s update by IPG Mediabrands Magna unit brings it down slightly, the U.S. currently appears to be on track to expand nearly 12% following one of its greatest expansion years ever in 2021, which benefited from a post-pandemic and recessionary recovery.

The initial outlook for 2023 also appears reasonably stable, although it has moved downward from the weight of Dentsu’s bullish July update.

Next year currently stands at a 4.5% consensus for U.S. ad expansion — which, given its comps with 2021 and 2022 and the absence of as much as $10 billion in incremental ad spending from cyclical events like the Olympics, World Cup and midterm elections, appears healthy in light of the overall economic uncertainty.

But as GroupM’s Business Intelligence team has been remarking in recent updates, as well as its weekly “This Week Next Week” podcast, ad spending has increasingly become decoupled from the macro economy, and there are new and emerging dark pockets of new ad spending that are constantly being discovered — from U.S. spending by Chinese companies targeting Americans, to the emergence of vital D2C categories, to a surge in retail media ad spending.

And while 2022 and 2023 may not experience the kind of “planetary realignment” that both IPG Mediabrands’ Vincent Letang and GroupM’s Brian Wieser described about 2021’s results when they jointly presented their year-end outlooks in December 2021, there are at least some planetoids aligning in a way that appears to be sustaining long-term advertising growth.

(13)