Is facebook a Screaming buy Or sell?

February 28, 2016

Introduction

this text is directed to the person investor concerned with reaching the best possible complete return. The perfect whole return will typically come from a true growth stock simply because a sooner rising firm is price greater than a slower growing company past, present and future. on the other hand, for that commentary to be authentic, a high rate of revenue increase should be constantly finished. generating and sustaining a excessive rate of revenue growth is the tricky section, as a result of even if there are a couple of companies capable of generating higher earnings boom rates, they’re rare.

moreover, there is one undeniable fact about authentic increase stocks that’s however hotly debated and argued about. in reality and truth, a pure unadulterated boom stock under the strictest definition is able to dramatically outperforming most blue-chip dividend paying stocks. the whole return variations usually are not subtle, they’re important and profound. then again, I contend it is usually an indisputable fact that the chance differential between investing in actual boom shares and blue-chip dividend paying stocks is equally as important and profound. extra simply said, investing for high increase is dangerous.

consequently, it logically follows that top-boom stocks are far more research, due diligence and continuous monitoring intensive. consequently, when investing in growth stocks I suggest you be prepared to position in the vital work and energy to keep up with the corporate, its business and the competitors. In a free market, opponents gained’t let a excessive-boom company keep the market to itself. subsequently, if the investor just isn’t keen to put in that effort, then investing in growth stocks may not be acceptable.

nevertheless, even if I simply renowned that investing in high-increase stocks is surely riskier than investing in blue-chip dividend boom stocks, their fast increase can successfully mitigate one of the crucial risk. thanks to the facility of compounding, the company that’s growing its earnings very fast can bail traders out despite the fact that they overpay for the inventory at buy. in fact, this assumes that the company continues growing salary at above-moderate charges. And more importantly, assumes that the investor stays the direction, which admittedly is an aggressive assumption.

the facility and safety of higher salary increase

With the above said, this text is primarily in regards to the energy, protection and return possible that may happen when investing in growth shares. despite the fact that I will be referencing facebook as a quintessential instance of a true unadulterated increase inventory, I contend that an prognosis of facebook, past, present and future also deals vital investing lessons about growth stock investing normally.

moreover, I consider myself a dedicated price investor. regular readers of my work will attest to the fact that I believe truthful valuation an important metric to believe before investing in any inventory. no longer best do I write about the significance of valuation in virtually every article I put up, i’ve even been given the name MisterValuation and likewise operate a site under that identify.

In the identical vein, I consider fair valuation a very important metric to imagine and review when selecting high increase stocks simply as I do another inventory. on the other hand, as I previously alluded to, you could be more liberal with valuation when a company’s earnings boom price is as excessive as facebook (FB) has carried out. In different words, as i will later illustrate, that you can if truth be told overpay when firstly investing in a excessive-growth inventory and nonetheless make an above-average lengthy-time period total return. You do take on extra risk by using doing that, but due to the ability of compounding, a high fee of cash increase can still generate a significant and above-moderate total price of return.

this is possible as a result of because of the ability of compounding, investing in boom shares can in effect compress time. In different phrases, as a substitute of taking a decade or more to double your salary in a slower rising blue-chip dividend growth stock, you can double your income so much quicker in a true boom inventory.

to illustrate my point i’ll turn to the widely recognized Rule of seventy two. This rule states you could calculate the number of years it takes to double your earnings (or your cash) at a given compound return by dividing it into the quantity seventy two. i’ve continuously utilized the next illustration to reveal the purpose i’m making in regards to the energy of compounding and the way it compresses time.

First i will make the assumption that the average individual has a working lifespan of 36 years. In brand new occasions this can be a conservative assumption, however as i’ll quickly illustrate, it helps the math. next i’ll think two totally different compound rates of salary boom as they practice to the common dividend increase inventory, after which to the pure increase stock. For the dividend growth inventory i will suppose a generous and above- average fee of salary increase of 10% once a year. For the pure boom inventory i’ll suppose the appropriately larger rate of salary growth of 20% per annum. the math then seems like this:

With the dividend boom stock, If I divide 10% into 72, I calculate that it’ll take 7.2 years to double my income (seventy two/10% = 7.2 years).

With the pure growth stock, if I divide 20% into 72, I calculate it’ll take simplest 3.6 years to double my salary (72/20%=3.6 years). In other phrases, income will double in half the time.

If I practice this math to my assumed reasonable working life of 36 years, I get the next results:

If my income double each 7.2 years at a ten% charge of boom, i’ll get 5 doubles in 36 years (36/7.2=5).

If my cash double every 3.6 years at a 20% charge of income boom, i’ll get 10 doubles in 36 years (36/3.6=10).

the net impact is that via doubling my moderate charge of cash growth from 10% to 20% per annum, I don’t generate two times the cash with the aid of rising at twice the rate. as a substitute, I get double the doubles. looked at from the viewpoint of the primary $ 1 (buck) of revenue, the ability of compounding (compressing time) turns into vividly clear.

Doubling my first greenback’s worth of cash 5 times at the 10% boom charge results in the next: $ 1 doubles 5 occasions to $ 2, $ four, $ eight, $ 16, and ultimately to $ 32. however, on the 20% boom charge I get 5 further doubles over the identical 36 12 months timeframe as follows: $ sixty four, $ 128, $ 256, $ 512, $ 1024.

to place this into perspective, over my assumed 36 12 months working lifetime I generate 32 instances extra salary through rising at 20% than i might have if my revenue grew at 10% (1024/32=32). Doubling the collection of doubles over the same timeframe presentations the fantastic energy of compounding that real increase stocks are in a position to providing.

alternatively, it will have to be cited that successfully rising earnings at the fee of 20% every year over a working lifetime is a uncommon and difficult feat. in the end the law of enormous numbers comes into play and an organization’s income growth charge will indubitably decelerate because of this. nonetheless, the above exercise is valuable for the insights it offers into the ability of compounding.

additionally, this information about compounding additionally ties in well to price of return expectations. i’ve evaluated and analyzed thousands of corporations in my lifetime. This expertise has led me to what I believe an plain conclusion. in the end, salary resolve market value. furthermore, as this pertains to achieving a excessive complete return, when a stock is purchased at a sound valuation, your total return will be highly correlated to a company’s cash growth achievement. To be extra exact, your capital appreciation part specifically shall be generated according to income boom. moreover, that is also authentic for dividend paying stocks. Capital appreciation will relate to income growth, and so will the profits part from dividends. In other phrases, a dividend paying stock’s rate of dividend growth will also highly correlate to its earnings boom.

the facility of Diversification When Investing In increase stocks

despite your investing strategy, diversification must always play the most important position. nevertheless, diversifying a boom inventory portfolio offers a distinct dynamic than is found with extra conservative investing methods. due to the ability of compounding at a excessive increase fee, a various increase inventory portfolio can produce robust results even when the portfolio comprises a big proportion of screw ups.

the following table presented for illustration functions assumes a $ 1 million portfolio invested in 15 high-boom stocks with roughly $ 660,667 invested in every. The assumptions offered within the table are extreme. for example, the primary column assumes that eighty% (12 out of 15) of the growth stocks go totally bankrupt and most effective 3 (20%) achieve the 20% return objective over 10 years. Even below this extreme and extremely not going circumstance, the portfolio would nonetheless achieve a positive whole return of 2.sixteen% annualized. of course, in the event you batted 100%, the portfolio would generate a total return of 20% every year.

the purpose of this train is for example that you simply most effective want just a few a success increase stocks in a portfolio to make a wonderful price of return. this is what I meant after I stated earlier that a excessive price of income increase can mitigate risk, particularly when the expansion stock portfolio is even somewhat diverse.

fb is a Quintessential example of a boom stock

note: earlier than I proceed on, i would like it to be clear that this article just isn’t meant to provide a comprehensive analysis of the industry or fundamentals assisting fb. as a substitute, this article is introduced on the thesis that that diagnosis and due diligence had already been completed. the principle premise and purpose of this article is to present, overview and speak about the mathematics at the back of what drives long-time period returns and how one can calculate them. on the other hand, here are two articles right here and here that offer fascinating insights into facebook’s future growth possible.

therefore, the above dialogue in regards to the arithmetic at the back of investing in growth stocks was once supplied to provide a clear viewpoint towards answering the question posed within the title of this article. Is fb a screaming buy or sell? the reply to this query is arguable, and i’m sure there will likely be readers that take either side. nevertheless, the correct solution for every individual investor shall be associated to their own non-public chance tolerances and typical investing behaviors.

My definition of a boom inventory is simple and precise. initially, a increase stock represents the in style inventory of a company whose trade is constantly rising earnings and cash waft at a significantly above-moderate charge. extra exactly, my definition of a growth inventory is a company whose cash are consistently rising at a minimal rate of alternate of earnings growth of 15% or higher.

alternatively, a hyper increase stock is one who I define as rising salary at a price of change of 25% or higher. Admittedly, despite the fact that each categories are rare, there are more 15% growers than there are companies growing income at 25% or better. In between these broader gradations of growth are extra growth categories corresponding to a high grower at 20%, etc. consequently, as i will subsequent illustrate, facebook represents a quintessential instance of a hyper increase stock.

the math assisting facebook’s historic performance

additionally, the above discussion was additionally provided as an instance that each one investing is ultimately about the math. To be clear, historic efficiency shall be a perform of how briskly the corporate has grown its trade, which is a exactly-measurable set of historical tips. the next revenue and price correlated F.A.S.T. Graphs™ evidently illustrates how facebook’s stock value (the black line) has tracked its income (the orange line) considering that 2013.

The graph additionally illustrates that fb has grown its revenue at the unbelievable charge of fifty.7% per yr. considering the fact that facebook has grown income above 15%, the system utilized to draw the orange valuation reference line is P/E ratio = to earnings boom fee (note: the system is depicted in the orange rectangle in the fast info field as P/E=G). subsequently, the orange line on the graph represents a P/E ratio or cash more than one of 50.7.

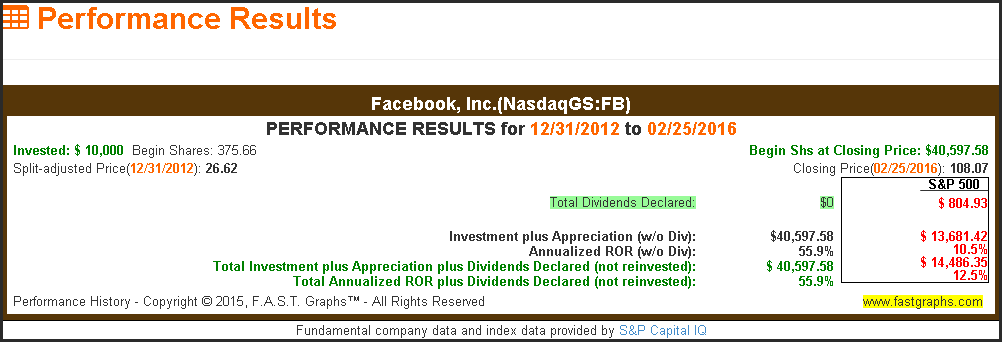

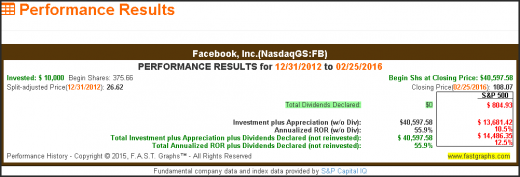

the following historic efficiency results for fb over this timeframe evidently validate my thesis that salary power market value. Had you invested $ 10,000 in facebook on December 31, 2012 that funding would now be value $ forty,597.58. That calculates to an annual fee of return of fifty five.9% which closely correlates to the company’s income increase price of 50.7%. at the end of the day, investing in popular shares is all about the mathematics behind the company’s working achievements.

Estimating fb’s Future performance can also be All about the Math

up to now i have illustrated how lengthy-time period facebook shareholders were rewarded in virtually direct proportion to its industry results. on the other hand, as I alluded to prior, historic performance is measurable because it has already passed off. then again, the future performance of fb is still an unknown. nonetheless, my argument is that facebook’s future efficiency may also be a function of the maths at the back of its future earnings boom.

additionally, at least over the intermediate-term, I proceed to consider that facebook might not be paying a dividend each time quickly. due to this fact, facebook’s future total return can even be a right away perform of capital appreciation generated with the aid of future salary boom. after all, for the reason that future is always unknown, it might probably handiest be forecast or estimated.

My recommendation is that buyers must run numerous forecasts according to cheap assumptions concerning facebook’s future increase. In other words, a couple of “what if” eventualities should be calculated with the objective of operating conservative, positive, average, and even worst case situations. but most significantly, present or prospective buyers must do the mathematics based on every of these eventualities as a way to calculate specific future return prospects. As in the past stated, the endgame of all a hit investing is always concerning the math.

Doing the math does not wish to be arduous in case you have the best tools at your disposal. Spreadsheets or financial calculators can do the trick. Regardless, I consider it’s imperative that traders do the mathematics as a way to have fairly actual calculations about what their future returns might be. subsequently, I provide the next video utilizing the quite a lot of F.A.S.T. Graphs™ “Forecasting Calculators” the place i will run more than a few “what if” scenarios and calculations on facebook’s doable future returns over the subsequent 3 to 5 years.

the key merit at the back of this course of is to realize as clear of a view and working out of fb’s future return potentialities in line with quite a lot of eventualities. individually, that is a long way superior to easily investing in a inventory with the hope that it is going to go up, or that you’ll make money. furthermore, this exercise is designed to provide an inexpensive range of chances and potentialities relating to future returns. I imagine this analogous to investing with your eyes vast open.

abstract and Conclusions

facebook is evidently one of the dominant (hyper) increase shares of up to date instances. Its historical cash growth achievements had been nothing in need of miraculous. as a result, the company has already grown to a market cap in way over $ 300 billion over a very quick time frame. this may be the biggest problem the corporate faces relating to its future growth attainable. nonetheless, the company continues to exceed consensus analyst cash estimates kind of like clockwork.

according to historical income achievements, fb appears reasonably valued despite its lofty present blended P/E ratio over 44. When looking to the future, it appears that fb would possibly continue to grow cash at 30%-plus charges, as a minimum for the following couple of years. therefore, due to the ability of compounding, fb generally is a profitable future investment even if the stock experiences P/E ratio contraction. the key of course is future earnings boom. At current valuations the company should continue to develop very fast to make stronger its stock worth. Is fb a screaming buy or promote? I leave that decision as much as you.

Disclosure: No place.

Disclaimer: The opinions on this report are for informational and educational functions best and must no longer be construed as a suggestion to purchase or sell the shares talked about or to solicit transactions or shoppers. previous performance of the businesses discussed may not continue and the companies won’t reach the earnings growth as envisioned. the guidelines in this file is believed to be accurate, however in no way must a person act upon the guidelines contained inside. we don’t counsel that anyone act upon any funding information with out first consulting an funding marketing consultant as to the suitability of such investments for his specific scenario.

trade & Finance Articles on business 2 community

(18)