Product listing ads, digital co-op and the $13 billion opportunity

By joining forces with brands, retailers making a PLA co-op spend can bid more aggressively and expand their profile where it matters.

In October my company, Crealytics, hosted a conference called [New York] Know Go. This one-day event focused on one of search marketing’s most exciting new chapters: the rise of digital co-op.

The day sparked numerous questions. What does the landscape look like for digital co-op today? How can retailers and their partners avoid its potential pitfalls? And why should we be so excited about a practice still shaking off a pre-digital hangover?

Stuck in the past

Co-op marketing has existed for a long time. Since the late 19th century, retailers have sought higher turnovers via marriages of budgetary convenience. Brands agree to share the cost of an ad with a retailer for more product exposure.

Spend two minutes looking and you’ll find examples of this collaboration everywhere: from billboards to catalogs and magazines to TV commercials. In fact, co-op’s profile feels disproportionately offline. Fully 80 percent of the world’s available co-op funds flow into non-digital channels.

But advertisers have woken up to digital co-op’s potential. For one thing, it promises brands a better understanding of where their budgets go. Unlike the co-op of old, a search marketing equivalent supports a cleaner, more accountable process. There’s also more potential for retailers, for whom PLA acts as primary sales driver.

Let’s look at the numbers.

Co-op’s overall market size stands at $70 billion. But just 20 percent of this is used for digital advertising. Additionally, we estimate that eCommerce pure players spend 80 percent of their budgets on digital channels. Applying this behavior to the wider market unlocks serious long-term opportunity. The gap (from 20 percent to 80 percent) closes. The industry sees a dramatic redistribution of co-op spend, mainly to digital. This leaves $42 billion up for grabs.

Thanks in no small part to its co-op fueled ad business, Amazon seem likely to claim around half of that amount. Meanwhile, Google and Microsoft Bing recently launched solutions that allow brands to subsidize a retailer’s PLA spend, increasing their marketing pressure and driving additional sales. Given these latest developments, we can assume that search marketing will swallow around 80 percent of the other half – about $16.8 billion. And product listing ads (PLAs) will soak up most of this figure. Even a rough estimate, let’s say 80 percent, puts future PLA co-op spend at more than $13 billion.

Amazon leads the race for colonization

Anyone who’s monitored Google and Amazon’s trajectory reaches a similar verdict. Once upon a time, Google was just a search engine. Amazon, a retailer. But the lines have blurred, as both increasingly reflect each other’s USPs. Things get especially intriguing when it comes to sponsored product models: a key piece of the co-op puzzle.

What are Amazon sponsored products?

Amazon’s sponsored products are keyword-driven, PPC ads that push traffic to a particular product page within Amazon’s own ecosystem. Crucially, these ads never link out. Brands that use them can boost their rankings…and drive additional sales.

The eCommerce giant clocked up over $2 billion in ad revenue…in just Q2 of this year. And its sponsored products accounted for over 80 percent of this figure, mainly thanks to small- and medium-tier Amazon sellers. This is in marked contrast to Google, which makes the bulk of its revenue from big brands and agencies.

Amazon recently extended the reach of its sponsored products offsite, via its Extended Ad Network (in the form of display retargeting). As a response, Google announced a co-funded Shopping Ads beta. And Bing has also joined the game, trialling its own co-op bid platform in the U.S. market.

We’re seeing a battle between Amazon on the one hand, and the rest of the retail market partnering with Google on the other. Amazon leads the game. Jeff Bezos’ empire remains larger than the rest of the retail market combined. So how do the latest moves in co-op advertising compare? Is Amazon strengthening its position? Or is the rest of the market catching up?

An era of co-opportunity

Advertisers prefer PLAs over text ads for many reasons. But with popularity comes competition. It’s now a highly competitive marketplace and, truthfully, many retailers struggle to afford the top positions. This prompts a domino effect for brands who sell through these retailers. Their products don’t show up, get squeezed out of valuable real estate and simply aren’t found.

Collaboration offers an antidote. By joining forces with brands, retailers have bigger paid search budgets to play with. They can bid more aggressively and expand their profile where it matters.

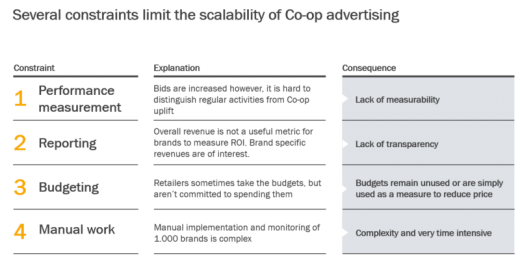

As with many early-stage systems, certain roadblocks have slowed PLA co-op’s path to scale:

To leverage PLA co-op, retailers and brands have several options:

Google and Microsoft Bing’s solutions offer brands the possibility to “boost” bids set by the retailer. Those digitally savvy enough can use the platform to manage bids on a granular level. Google then provides the estimated incremental impact via dedicated reporting. The lure of full control is highly tempting. Time, effort, and the risk of not hitting targets can stagnate many brands.

Because a brand can easily allocate their budget across several retailers, freedom of choice ensures that no one retailer can monopolize a brand’s entire budget. This completely levels the playing field for brands and retailers alike.

Alternatively, following a new and sophisticated methodology presented at [New York] Know Go, retailers can manage co-op PLA campaigns for their brands directly.

This sees the retailer leverage its relationships, acquire the brand’s budgets directly and manage campaigns towards specific targets. Such an approach implies that the retailer reallocates 100 percent of retargeting spend to prospecting. Meanwhile, the brand can retarget select audiences like website visitors, audiences similar to website visitors, or in-market audiences.

Opinions expressed in this article are those of the guest author and not necessarily Marketing Land. Staff authors are listed here.

About The Author

Andreas Reiffen is an entrepreneur, marketing technologist and thought leader in data-driven advertising. Between 2006 and 2008 Andreas operated as a PPC super affiliate working for Zappos and other retailers. In 2008 he founded crealytics, the Berlin-based provider of camato, the leading Google Shopping Tool to automate PLA campaigns and improve performance. Several of the largest international Ecommerce retailers are using camato to manage Google Shopping in more than 100 markets across the globe, generating over $3B in revenues per year. camato has been shortlisted for numerous awards in 2016 including European Performance Marketing and Drum Search.

Marketing Land – Internet Marketing News, Strategies & Tips

(69)