Red vs. Blue Ocean Strategies

It can be difficult to succeed with the cutthroat competition in the business environment today. Luckily, there are many strategies you can use in order to gain an edge on your competition. Two of these are red ocean and blue ocean strategies, which were introduced by W. Chan Kim and Renée Mauborgne in 2005.

Red Ocean Strategies

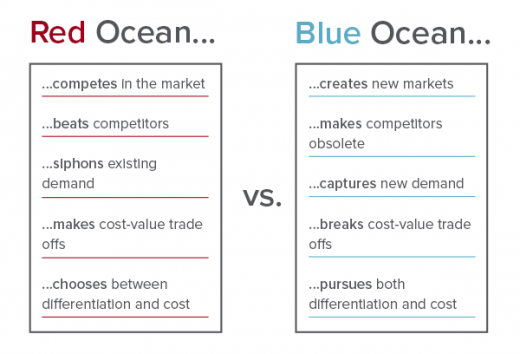

A red ocean strategy involves competing in industries that are currently in existence. This often requires overcoming an intense level of competition and can often involve the commoditization of the industry where companies are competing mainly on price. For this strategy, the key goals are to beat the competition and exploit existing demand.

“The key goals of the red ocean strategy are to beat the competition and exploit existing demand.”

One industry in which a red ocean strategy would be necessary is the soft drink industry. This industry has been in existence for a long time, and there are many barriers to entry. There are industry leaders in place such as Coke and Pepsi, and there are also many smaller companies also in competition for market share. There’s also limited shelf space and vending spots, well-established brand recognition of popular, current brands, and many other factors that affect new competition. This causes the soft drink industry to be very competitive to enter and succeed in.

Blue Ocean Strategies

A blue ocean strategy is based on creating demand that is not currently in existence, rather than fighting over it with other companies. You must keep in mind that there is a deeper potential of the marketplace that hasn’t been explored yet. Most blue oceans are created from within red oceans by expanding existing industry boundaries. The key to a successful blue ocean strategy is finding the right market opportunity and making the competition irrelevant.

“The key goals of the blue ocean strategy are finding the right marketing opportunity and making the competition irrelevant.”

An example of a successful execution of a blue ocean strategy is the iPod. When the iPod was introduced in 2001, Steve Jobs said that “with [the] iPod, Apple has invented a whole new category of digital music player that lets you put your entire music collection in your pocket and listen to it wherever you go.” Apple looked beyond what was in the market at that time and introduced a product that created a new industry in and of itself. Apple looked beyond what customers were asking for and created a successful product.

The Winning Strategic Approach

While the authors of Blue Ocean Strategy suggest using the latter approach, no matter which you select, there are a few things to keep in mind. First of all, it is important to remember that value creation and innovation are critical success factors. Also, remain aware of the industry that you are competing against as well as new introductions to the market that may disrupt any market share that you have attained.

Business & Finance Articles on Business 2 Community

(45)