Retirees: i didn’t buy IBM to promote, It’s concerning the Dividend profits silly

October 27, 2015

Introduction

there are lots of investing methods and rules that retired buyers can make the most of to cut back the risk related to investing in equities (shares) for his or her retirement portfolios. choosing to spend money on the best quality stocks your mind can conceive sits at the high of the checklist. there are numerous elements that traders can analyze and examine to resolve whether or not an organization is top quality or now not.

the principle determinant of high quality is advanced financial energy. Financially robust corporations possess the staying power and tools to climate the occasional dangerous storms a good way to inevitably happen. every industry will once in a while face challenges and difficulties. meeting those challenges requires a robust steadiness sheet and an adaptive and capable management group to information the company across bothered waters.

Evaluating monetary power may also be entire throughout the examination of some easy but essential elementary metrics. fortunately, much of that work is already finished for us by using centered and respected reporting companies reminiscent of usual & terrible’s, worth Line, MorningStar, and so on., in the type of credit score scores.

there are many to be had sources the place retired buyers can to find that information. the bottom line is to look for firms which might be awarded what is mentioned in monetary circles as investment-grade scores. in most cases, the businesses with the best ratings could have a capital A or higher of their credit standing.

Retired traders concerned with security can dig deeper through inspecting necessary fundamentals comparable to cash waft, free money glide and debt levels. mentioned overly-simplistically, you are going to be in search of firms that have the power of cash flows to enhance debt payments and present and future dividend distributions. concerning safety concerns, cash flows are more relevant than cash. as a result of when it comes to the survival of a trade, cash glide is king. because it relates to security, a industry surviving as an ongoing concern is the ultimate line of protection.

additionally, in the case of figuring out the safety associated with investing in a stock, figuring out whether it possesses superior financial power is an obvious and regularly-utilized method. on the other hand, there are extra essential security measurements that are more delicate, much less understood and often either disregarded or their significance no longer given the credit score deserved.

These more delicate security measurements are an above average, but sustainable, present dividend yield and sound valuation, or higher yet, significant undervaluation. the remainder of this text will observe the monetary potential and these two important however more subtle security measurements as they follow to the a lot-maligned blue-chip stalwart IBM.

IBM’s monetary potential

IBM was based in 1910, and included within the state of new York in 1911. the company took on the enduring IBM name in 1924. consequently, IBM has been an American technology stalwart even sooner than technology became cool. As such, IBM has been lengthy-in demand as a blue-chip dividend increase stock. so much so that legendary investor Peter Lynch as soon as quipped “no person ever gets fired for getting IBM.”

listed here are IBM’s credit ratings from 3 respected Sources:

same old & bad’s: AA-

MorningStar: AA-

price Line: AA+

IBM Liquidity Ratios

IBM’s present ratio (crq) is and has been above 1, indicating that the corporate is fully capable of paying its responsibilities. IBM’s fast ratio (qrq) also supports its capacity to meet short-term obligations. Importantly, both of these ratios continue to remain within IBM’s historic norms.

IBM’s Dividend Yield, record and Sustainability

in the title of this article I ironically integrated the phrase “it’s concerning the profits stupid.” on the other hand, I was now not in basic terms attempting to be sardonic, because that phrase represents a significantly essential theory about investing in huge blue-chip dividend growth stocks. in spite of whether or not you’re investing in revered blue chips akin to Johnson & Johnson (JNJ), Procter & Gamble (PG), Coca-Cola (KO), or IBM (IBM), and so forth., it will be naïve for your section to believe you will mechanically or at all times outperform the market on a complete return foundation.

Behemoths equivalent to these described above have simply develop into too huge to develop quick. Their main enchantment derives from their security characteristics and the dividend earnings they’ve produced previously, and are able to offering at some point. on this regard, it could now not be naïve to believe that these blue-chip dividend stalwarts might produce considerably more future dividend profits than the final market, as a result of in truth and historic fact, they all have – IBM incorporated.

mentioned extra directly, investing in blue-chip dividend increase stocks isn’t about how so much their stock value might savour. as a substitute, it’s about their safety and how much dividend earnings and dividend income boom they may be able to present retired buyers long into the future. alternatively, this is not to indicate that they don’t possess the capability for capital appreciation, because they all do. this is very true if they’re bought at sound or horny valuations. i will talk about the importance of sound and attractive valuation in additional element later.

This brings me to a selected dialogue about IBM and its dividend history. This blue-chip stalwart has paid its stockholders a dividend annually, in truth, each quarter, because 1916. moreover, it has elevated its dividend for the prior 20 consecutive years at a fee of approximately 15% each year. As an important aside, this dividend increase rate is significantly better than its historical income increase rate.

IBM’s Dividend increase 1995-2014

a part of this may also be attributed to the truth that its payout ratio has often increased from a low of 12% in 1996, to its 2014 payout ratio of 26%. but most importantly, IBM’s low payout ratio coupled with its robust free money float generation means that above-average dividend boom is prone to continue lengthy into the longer term. When investing in IBM on your retirement portfolios, it’s all in regards to the profits.

when you observe the following performance outcomes on IBM for the reason that December 29, 1995, I direct your attention to two essential columns. the first column to study is “Dividends per Share” the place one can find the constant and demanding boom of their dividend price per share for each year. The 2nd column I recommend you focal point on is “Dividends Declared.” With this column you are going to see the annual growth of dividend earnings in line with an unique $ 10,000 investment. I contend that that is the primary reason for considering IBM for your retirement portfolios.

subsequent is the consideration of IBM’s excessive present yield of approximately 3.7%. this is significantly above the current yield of 2.2% for the S&P 500. in addition to the obvious profits merit, an above-average present yield also serves as crucial safety attribute. In concept and principle, each dividend payment you receive from a dividend boom stock technically reduces the amount of capital you will have at risk. larger-yielding shares like IBM are in essence decreasing your risk every time they ship you a dividend check. This minimization of risk is principally related when the above-reasonable yield funds are rising as fast as they are with IBM.

the next F.A.S.T. Graphs™ plots IBM’s historic present yields since 1996. notice that that is the absolute best current yield that IBM has provided shareholders over that timeframe. in addition to the benefits cited above, that is additionally the most important valuation dimension. IBM’s current valuation can be elaborated on more totally in the subsequent section.

In his ebook “the one absolute best funding-earning profits with Dividend boom” cash supervisor Lowell Miller presented his easy method for deciding on his idea of a potential single best investment candidate as follows:

“high quality

+ excessive present Dividend

+ excessive growth of Dividend

= high whole Returns”

From what i have offered thus far, IBM qualifies beautifully. then again, when you consider that I’m sometimes called MisterValuation it’s vital to me so as to add truthful or sexy valuation as a further metric to Mr. Miller’s formulation. even though I agree that the above three characteristics that Mr. Miller deals are necessary, and really more likely to result in high complete returns, I contend that those returns shall be better and the risk decrease when honest or horny valuation is brought to the equation. due to this fact, with all due appreciate to Mr. Miller, i’d individually revise his system as follows:

top of the range

+ high present Dividend

+ high increase of Dividend

+ sexy Valuation

= excessive total Returns

Now that I’ve reviewed IBM’s dividend yield and historic record, it’s time to maneuver on to the necessary dialogue of IBM’s dividend sustainability. As I previously instructed, cash float is “king” when evaluating the sustainability of an organization’s means to pay its dividend. the next enjoyable Graph (basic underlying numbers) plots IBM’s cash glide per share (cflps), levered free cash flow per share (lfcflps) and dividends paid per share (dvpps) from 1995 to 2014.

a quick examination of this graph illustrates that IBM’s dividend has been greater than competently lined by way of its prodigious cash drift generation (observe: levered free cash drift is after interest on debt has been paid). And most likely extra importantly, the graph illustrates that there is quite a lot of room for IBM to pay even larger dividends if administration considered it acceptable.

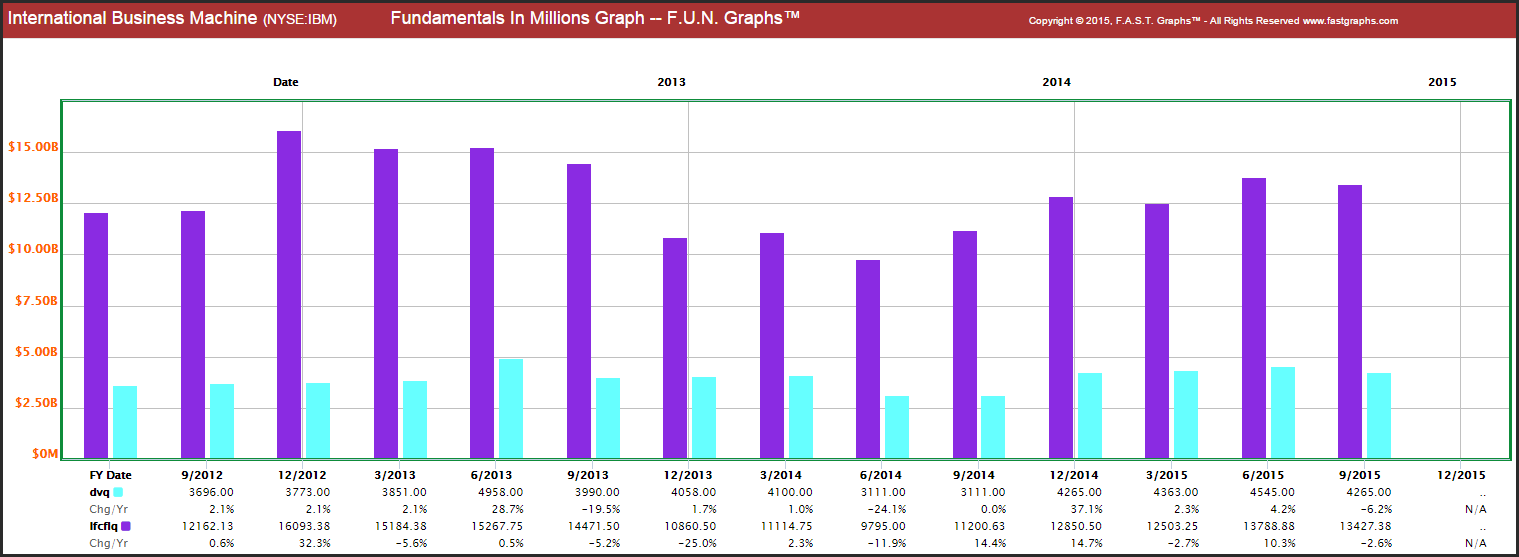

This next graph items levered free money waft (lfcflq) and dividends (dvq) in tens of millions of bucks for the remaining a number of quarters to incorporate their most recently completed quarterly record for the length ending September 2015. despite the fact that IBM has been a great deal maligned through many pundits, it is clear to me that levered free cash go with the flow continues to fortify their dividends.

IBM’s current Valuation

in accordance with my many years of expertise investing in well-liked stocks, i’ve concluded that assessing truthful valuation is a main consideration investors should at all times try and make. stock markets are auctions and due to this fact inventory price actions are driven by means of provide and demand in the shorter run. consequently, stock prices may also be pushed both dramatically above or under honest value at any second in time. on the other hand, in the longer run, inventory prices are pushed via the basic energy and performance of the business at the back of the stock.

due to this fact, the day-to-day gyrations of inventory costs can lead buyers into making short-term mistakes which are most often pushed by the emotions fear or greed. on the other hand, traders will have to remain acutely conscious that the short-time period will inevitably evolve into the long-term. because of this, in case you overpay for a stock in the quick run, you might be highly likely to either lose money or expertise bad lengthy-term performance that doesn’t compensate you for the danger you’re taking.

In distinction, if you purchase a inventory below its intrinsic value, you might be more likely to earn returns which are even better than the operating efficiency of the company within the longer run. but easiest of all, shopping for at low valuation reduces your long-time period risk at the similar time. alternatively, so as to succeed in these higher returns at decrease ranges of chance, it requires patience and an working out of the corporate’s monetary potential.

as soon as a standard inventory has momentum both up or down, that momentum can proceed for a time frame. unfortunately, they don’t ring a bell on the top or backside of a market. due to this fact, an overrated inventory can continue to rise quick-term, just as an undervalued inventory can proceed to fall within the shorter run. unfortunately, there’s no solution to predict upfront the precise second or stage when that might trade. due to this fact, you need to be affected person and belief fundamentals greater than worth action with the intention to benefit from investing at low valuations.

the next earnings and worth correlated F.A.S.T. Graphs™ on IBM clearly illustrates that stock worth has fallen considerably farther than up to date susceptible revenue justify. whereas many are traumatized by means of the losing stock worth over the past few years, I see nothing but probability. Having the chance to invest in a fantastic blue-chip like IBM at a P/E ratio less than 10 and a growing present dividend yield of 3.7% does no longer present itself very regularly. As an investor looking for safety and yield, I find IBM at present irresistible. when you consider that I’m not investing to sell IBM, my center of attention is on the neatly-lined and growing dividend yield.

moreover, once I review IBM based on cash flows, the picture is rather more sanguine. As viewed above, revenue have been beneath pressure, however money float era has remained strong. despite the fact that cash are the primary driver of stock price, money waft is the main supply of a company’s capability to generate persevering with dividends. I see no possibility to IBM’s dividend presently.

A growing Dividend income move was My goal for Investing In IBM

i’ve been, and continue to be aggressively including IBM into retirement portfolios. alternatively, even upon my first foray into the corporate, I used to be never anticipating large capital appreciation, at the least over the brief to intermediate time period. as a substitute, my angle about investing in this firm was primarily based completely on the chance to obtain a secure, above-reasonable and growing dividend yield. On that foundation, IBM has proven to be a powerful success because, as I anticipated, IBM’s dividend profits has frequently increased.

In the same context, i didn’t spend money on IBM with the theory of marketing it. as a substitute, my goal used to be to turn into a permanent, lengthy-term shareholder/proprietor of this dividend increase stalwart. when I invest in dividend increase shares for retirement, I at all times do it with an extended-time period view. My minimal definition of the lengthy-time period is a complete industry cycle; this is most often 3 to 5 years.

however, even if 3 to five years is my minimal definition of long-term, it’s not my ideal funding purpose. My best funding function is to own an organization completely. I don’t put money into the inventory market, I put money into what I consider are nice companies, purchased at sound and attractive valuations, that I are expecting to own perpetually.

as a result, as soon as i’ve laid my money down, I pay little or no attention to its inventory price action. due to the fact I have no intention of marketing, what the market is pricing my firm at is of absolutely no importance to me. alternatively, due to the fact i’m basically considering earnings as of late, the current stage, consistency and boom of the dividend fee is of paramount importance. as long as the dividends keep coming in, i’m satisfied and believe the funding a hit. And even higher, so long as they continue to develop, i’m meeting and exceeding my goals, and subsequently, fairly happy with my resolution.

as soon as once more, in that regard, IBM has been a resounding success. furthermore, I consider the fact that its worth has continued to float lower an incredible plus. After the long bull-run within the normal inventory market we have not too long ago loved, it has develop into slightly uncommon to seek out high-quality dividend increase stocks at sexy price. within the face of lately’s low rates of interest, yield hungry traders have driven the values of most quality dividend increase shares too excessive.

i’ve penned three articles on IBM on the grounds that could 2012 found here, right here and right here. for the reason that publication of my first article, IBM’s stock value has drifted down approximately 27%. however, IBM has remained profitable over this timeframe, however admittedly revenue per share have no longer grown. In contrast, cash drift per share has endured to develop, albeit at a quite low rate. nevertheless, this continues to present me confidence that IBM’s dividend is secure and in a position to persevering with to grow.

abstract and Conclusions

My case aiding investing in IBM is totally predicated on its generous current yield and my view of the protection and sustainability of its trade. there is not any shortage of sure and terrible articles or stories throughout numerous financial blogs on IBM. some of them include vital information, but in my judgment, most of them symbolize merely the opinions of others. in my opinion, I want details over opinions.

I just lately watched an interview with Ginni Rometty, chairman, president and chief executive officer of IBM and she shared some somewhat startling tips about the company. Responding to the query is IBM cool? – she offered the following, which I paraphrase:

If it’s cool that 90% of the banks on the earth run on IBM, then IBM is cool. If it’s cool that eighty% of the airlines on the planet run on IBM, then IBM is cool. If it’s cool that 60% of all of the transactions in industry in the world are achieved by IBM, then IBM is cool.

IBM is an entrenched know-how stalwart and bellwether that possesses a large moat in keeping with its large and centered customer base. the corporate is at the moment engaged in a transformation to stay current within the hastily changing technology setting. this isn’t the first time that IBM has been required to do this in their storied previous. Odds are, it received’t be the ultimate. as a result, i’d refrain from attempting to place an exact number on IBM’s means to develop going forward. then again, I do believe that increase continues to be of their future. because of this, i admire IBM for its safety, high and rising dividend yield and its low valuation relative to its fundamental potential.

Disclosure: lengthy IBM.

Disclaimer: The opinions on this report are for informational and academic purposes simplest and will have to now not be construed as a suggestion to buy or promote the shares mentioned or to solicit transactions or clients. prior efficiency of the businesses mentioned may not proceed and the businesses may not achieve the salary growth as predicted. the tips on this document is believed to be accurate, however in no way will have to a person act upon the guidelines contained within. we do not counsel that someone act upon any funding data without first consulting an investment advisor as to the suitability of such investments for his specific situation.

industry & Finance Articles on business 2 neighborhood

(149)