The adtech trends rounding out 2019: Programmatic growth, measurement standards, privacy implications

Looking to 2020, adtech players can expect new capabilities driven by a customer-first approach grounded in privacy, brand experience, and standardization.

As the digital landscape continues to fragment, advertisers are looking for more ways to reach customers with one-to-one messaging that drives a lasting impact. As digital ad capabilities become more accessible and effective, both the sell-side and buy-side are shifting to embrace more advanced solutions.

In particular, programmatic advertising (digital display, advanced TV, digital out-of-home) has reached unprecedented adoption in recent years as the industry responds to changing marketplace dynamics. Powerful third-party platforms and tools have enabled advertisers to expand the efficiency and effectiveness of media programs, even as the complexity of the programmatic value chain evolves.

With all the progress of advanced digital advertising, it’s easy to lose sight of big-picture trends and insights. From enterprise consolidations that impact ad operations to recent advances in supply chain transparency, the advertising solutions of our modern digital age are vast and everchanging. But how are these changes affecting the digital ecosystem? And what can advertisers expect in adtech for the year to come?

Here are the top adtech trends rounding out 2019.

Programmatic growth continues, with duopoly dominance

Since the advent of programmatic display over a decade ago, the adtech industry has seen enormous growth, with programmatic now representing the primary method of buying digital media in the U.S, according to eMarketer. In fact, eMarketer estimates US advertisers will spend nearly $60 billion on programmatic display by the end of 2019. By 2021, nearly 88%, or $81.00 billion, of all U.S. digital display ad dollars will transact programmatically, says the research firm.

Duopoly’s growing share. By the end of 2019, the combined ad revenues of Facebook and Google’s media in the U.S. will account for more than half of advertisers’ total budgets for programmatic display, eMarketer predicts. That portion will increase in 2020, with Facebook and Google accounting for nearly 63% of ad spend next year.

Amazon steps up

Overall, digital ad spend in the U.S. remains dominated by Google and Facebook. Amazon (at 7% share) is the only seller to break out from the pack of would-be challengers.

Amazon this year released a number of improvements to its ad-buying interfaces, such as improving the usability of its DSP, extending the reach of Sponsored Products, adding a rewards program tool, incorporating customer acquisition metrics and enabling dynamic bidding for Sponsored Products ads.

However, even as Amazon continues to build up its advertising product, as well as the new mobile, over-the-top (OTT) and connected TV ad inventory entering the space in the coming year, the Facebook/Google duopoly will likely continue to dominate into 2020.

According to WARC’s Global Ad Trends report earlier this year, Google and Facebook’s advertising authority can be attributed back to the paid search and social ad units that marketers have found so successful. Additionally, the ease of use of these respective platforms make Facebook and Google’s ad products accessible at nearly every business scale, from SMB to enterprise.

High-quality creative is king

With the surge in digital growth, and brands have eagerly delivered on the demand for high-quality digital customer experiences. But CX has moved from a disruptive concept to a fundamental component of most digital strategies, resulting in advertisers seeking new ways to capture and retain customers.

Most digital ad experiences look, feel, and behave in a similar fashion – and consumers have come to expect it. According to Pattisall, many marketers recognize this issue of “sameness,” and it’s prompted a re-emergence of creative as a fundamental priority for advertisers.

“In our pursuit to be customer-centric marketers – to answer every customer need, want, and desire with digital – we have forgotten an important ingredient: creativity,” said Forrester principal analyst Jay Pattisall in a Forrester report earlier this year.

Industry moves to ramp up creative capabilities. A blog post from CMO by Adobe cites examples of the industry shift toward more creative-focused solutions to bolster digital advertising efforts.

In recent years, Accenture Interactive has been on a creative acquisition spree, acquiring agencies Droga5, The Monkeys, Karmarama, and Fjord in an effort to advance its creative capabilities. Similarly, Deloitte has expanded its creative foundation with the acquisitions of Acne and Heat.

We’ve also seen advances in the creative tools advertisers and marketers use to support ad efforts. For example, Adobe Asset Link, the extension that connects Adobe Experience Manager (AEM) assets to the Adobe Creative Cloud, has added integrations designed to streamline creative production. and create more efficient collaboration between marketers and creatives.

It’s expected that these moves to drive up creative will trickle into 2020, with more advertising agencies advocating high-quality creative over customer acquisition numbers and statistics.

The rise of dynamic creative. The race toward programmatic has put creative on the back burner, but now the adtech industry is pivoting to make quality creative more accessible with dynamic creative tools. For marketing and advertising to be successful, the creative and messaging must be the focal point. Today’s dynamic creative capabilities driven by machine learning mean that advertisers can programmatically serve ads that feature products, messaging, and creative that’s distinctly customized to each consumer.

Dynamic creative optimization (DCO) continues to be a powerful tool for advertisers to connect with consumers on a global scale, providing the ability to layer user-level data with targeted messages for each purchaser. And while large-scale personalization and targeting was once prohibitively complex, time-consuming, and costly, today’s DCO solutions make it automated and simple enough to deploy for virtually any campaign.

Connected TV driving significant growth

The dramatic shift to digital is spurring a new wave of investment in connected, or over-the-top (OTT), TV advertising. With better tools to programmatically target and measure ads across all screen types – think advanced TV and targeting capabilities – eMarketer predicts U.S. advertisers will buy $3.8 billion in programmatic TV ads in 2019 – a 236% increase from 2018.

Additionally, TV streaming is expected to grow tremendously in the coming years as audiences move away from costlier linear TV alternatives. In fact, by 2022, 60.1% of all US TV users will use over-the-top streaming platforms at least once per month, eMarketer predicts.

Despite the array of challenges still present in programmatic TV ((privacy, measurement, and transparency), connected TV campaigns that allow for precision targeting through granular consumer data are now more readily accessible to advertisers.

Advertisers moving to consolidate media partners

As tech continues to curve in favor of ease and efficiency, we can expect that platforms will consolidate to provide customers with more addressable solutions as the demand for ease and efficiency grows.

From MediaMath’s aggressive acquisition fundraising in 2018, to Amazon’s purchase of Sizmek’s ad servers earlier this year, and even Taboola and Outbrain’s recent merger, it’s clear that the adtech market is prepared to deliver more end-to-end advertising solutions.

Laser-focused on full-funnel data. The combined data of DMPs, CDPs, CRMs, DSPs and measurement platforms fuel advertisers’ efforts to boost ROAs with personalized targeting that reaches every step in the customer journey. As a result, rival platforms are coupling up, while other platforms are seeking ways to round out their offerings in an effort to offer a more integrated data hub.

Adtech consolidation is good news for programmatic media buyers, especially since integrating multiple platforms means less coordination, and lowers the possibility of bidding against oneself.

But other adtech players have recognized that the idea of a market dominated by a small number of conglomerates could drive up costs, resulting in less control for advertisers and fewer platforms to choose from.

“Google and Facebook have a forceful hold on today’s digital-advertising industry, meaning brands can’t walk away from them,” wrote John Nardone, CEO of analytics company Flashtalking, in a Forbes article earlier this year. “There is an urgent need to start building a more open ecosystem where brands have greater choice and more control.”

Increased focus on measurement and the value of inventory

Digital advertising as we know it was built on a foundation of open standards, where no single governing body regulates market transactions. But as adtech matures, advertisers and brands are demanding more standardized ways of measuring the effectiveness of ads funneled through the ad exchange.

Likewise, publishers are making more efforts to understand the value of their ad inventory. Viewability has become a key metric that helps define the value for both advertisers and publishers.

Viewability tracks ad impressions that appear “in-view” on a screen while having an opportunity to actually be seen by consumers — as opposed to impressions served, which may load on a page but never enter the user’s view. For publishers, selling inventory on a viewability basis enables publishers to offer higher-quality inventory at a competitive cost in the market.

On the demand side, advertisers are pushing for cross-screen and cross-platform measurement standards that can inform ad serving decisions. In August, Google adopted the IAB Tech Lab’s Open Measurement standard for mobile ads, providing advertisers with code libraries for facilitating third-party access to measurement data.

“The sell-side has been adopting OM quickly, and we ask brands, agencies, and Demand Side Platforms (DSPs) to get more active and take advantage of what [Open Measurement] offers.” said Dennis Buchheim, EVP and general manager of the IAB Tech Lab, at the time of the announcement.

Pubmatic’s Quarterly Mobile Index report from Q1 2019 showed Android devices making a drastic shift in ad budgets from RTB exchanges to private marketplaces (PMPs) to help maintain brand safety and protect against pilfering and the other fraud-related activities that exist in RTB.

Apple’s iOS devices show significantly lower PMP investment, which is expected given Apple’s staunch efforts to prioritize user privacy and tracking behavior. For Android devices that operate in an open-source environment, the dramatic shift to private marketplaces indicates a mounting focus on measurement standards and authorized inventory.

Ad fraud, privacy laws increasing the value of authorized data

Fraud prevention tightens. Financial losses from ad fraud have finally hit a slowdown, according to a report earlier this year by the Association of National Advertisers (ANA) and cybersecurity firm White Ops. The report predicted ad fraud losses would total $5.8 billion globally in 2019 – an almost 11 percent drop from the $6.5 billion global loss reported in 2017.

But even so, efforts to thwart ad fraud haven’t occurred overnight. Publishers have been moving vigorously to implement brand safety measures like ads.txt and brand controls – proving that these concentrated efforts are playing a hand in the decline of fraud.

Ads.txt default. In April, Google introduced new brand safety-focused initiatives, including defaulting to ads.txt inventory, supporting app-ads.txt and providing a central hub for brand controls in the interface. It meant that only publishers that have adopted the standard and have placed ads.txt files on their sites will be eligible for bids from DV360.

As part of the industry-wide effort to mitigate fraudulent ad selling, Centro, AdMob, and other demand platforms enforced ads.txt earlier this year.

Protecting advertisers and consumers. Adtech players have been making moves to bring user privacy and authorized inventory together under bundled solution offerings. And with CCPA on the horizon, the industry is eager to cover its bases to avoid privacy-related violations.

MediaMath, for example, launched SOURCE earlier this month – a media supply chain framework that aims to deliver full transparency, modernize commercial terms, and improve tech standards across the programmatic advertising ecosystem. AT&T’s advertising marketplace, Xandr, also announced a partnership with clean.io to reduce malicious advertising for publishers, end-users, and advertisers.

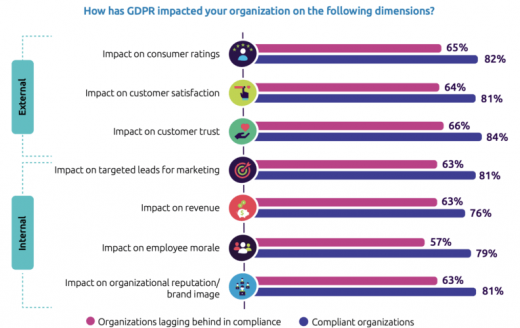

User privacy transforming tech ecosystem. Privacy compliance is also driving a shift in adtech capabilities with more built-in tools and solutions to help brands maintain compliance. A report from European consulting company Capgemini found that companies who meet GDPR compliance standards are outperforming non-compliant companies across a wide range of metrics.

The California Consumer Privacy Act (CCPA), expected to be live in the second half of 2019 and is set to extend the reach and powers of last year’s GDPR. In particular, it will expand upon consent requirements for website cookies. With an opt-in section for sites tracking those cookies.

To pursue ROAS in a digital world, advertisers are tracking behavior, targeting individuals, disrupting journeys, gathering data, and performing identity resolution. But as consumers take more ownership over their data and privacy rights, these strategies won’t be sustainable forever.

With the impact of browser actions on tracking Apple ITP, Google Chrome cookie blocking, and others, more platforms are taking measures to protect against bad actors. As a result, advertisers should prepare to embrace a wider array of holistic adtech solutions focused on brand safety and privacy compliance to support more accountable and effective advertising efforts.

Looking ahead: The big picture

In the next year, advertisers should expect changes in all of these areas, from creative resurgences to tighter measurement standards and growing consolidation among media partners. Players on both the buy-side and sell-side are making strategic shifts as consumer behavior, digital regulations, and technical capabilities evolve at record pace.

For advertisers and publishers alike, the coming year will present new opportunities driven by a customer-first approach grounded in privacy and brand experience. It will be important for advertisers to actively monitor and understand the big-picture changes happening in the adtech landscape as it surfaces new opportunities to connect brands with consumers.

About The Author

Taylor Peterson is Third Door Media’s Deputy Editor, managing industry-leading coverage that informs and inspires marketers. Based in New York, Taylor brings marketing expertise grounded in creative production and agency advertising for global brands. Taylor’s editorial focus blends digital marketing and creative strategy with topics like campaign management, emerging formats, and display advertising.

Marketing Land – Internet Marketing News, Strategies & Tips

(75)