The Many Faces of Open Banking: Australia, the U.K., and Japan

The Many Faces of Open Banking: Australia, the U.K., and Japan

Open Banking presents broad opportunities for fintech across the globe, and every region has its own specifics. For today’s research, we chose three countries from different parts of the world: Australia, the U.K., and Japan. In each country, Open Banking has its own history of development. Yet, all three are ready to adopt new regulations and bridge the gap between fintech and banks. Here are the many faces of open banking in Australia, the U.K., and Japan.

Fintech Regulations around the Globe: What is Going on Right Now?

Slightly Slow yet Thoughtful Launch in Australia

Initially designed to regulate personal data handling, Open Banking regulations have evolved in Australia recently. In addition to banking data, consumers now can share info on their loans and mortgages.

The Australian Competition and Consumer Commission regulates the activities of four major banks: Nab, CommBank, ANZ, and Westpac. Also, it issues accreditations for financial companies (including fintech) that decided to adopt new regulations.

Open Banking’s massive launch should strengthen fintechs’ position against the Big Four’s dominance. Currently, the major Australian banks have roughly 95% of the market share.

Per the last ACCC’s report, only two financial companies received accreditation, and the other 39 are still getting it. Though the authorities postponed the “public rollout” of Open Banking due to privacy and security concerns, the pandemic precipitated the transition. The major Australian banks and governments have already made some progress since the outbreak.

The Australian Treasury believes that Open Banking should help individuals and SMEs recover from the pandemic’s disastrous economic impact. Better data sharing can facilitate finance management and minimize banking costs to ensure a faster recovery.

Tremendous Progress so far in the U.K.

Open Banking began its history in the U.K. in 2016. In August of that year, the Competition and Markets Authority (CMA) issued the retail banking report. The report explicitly underlined that the financial sector was ripe for innovation.

Overcomplicated fee structures and account opening procedures for Small to Mid-sized Enterprises (SMEs) were among the main causes for the need.

As a counter to these procedures, the CMA proposed a set of retaliatory measures. One of those measures was an open API banking standard for sharing consumer data.

The first pivot to the new regulations was Open Banking Implementation Entity, a non-profit group of banks, fintech, SMEs, and others. Its goal was to ensure the security of financial record-sharing. However, Open Banking’s rollout began only in January 2018, when banks acquired the actual ability to share consumer data.

From that moment, third parties with access to consumer data have been encouraging consumer payments in different ways. Some provided universal services that allowed consumers to access their accounts in several banks (if they had such). They could access banking information through a single provider or from a single app. Other providers offered automated budgeting, cheaper overdrafts, and more features.

Big Initiatives in Japan Lead to Big Discoveries

Japan was among the first Asian countries to establish its own Open Banking framework. In 2015, Japan’s Financial Services Agency (FSA) established a consultation desk to make payments more accessible. However, the initiative was just the premise of Open Banking.

In the next couple of years, the Bank of Japan amended the Banking Act two times. In 2017, it changed the number of ownership banks must have in fintech. Next, it released a framework for regulating e-payments. In 2018, the FSA opened the Strategic Development & Management Bureau to devise a new financial services strategy with fintech as the “driving” initiative.

Japan’s economy relies heavily on cash, with banks focusing on cashless transactions and digital payments. The demand for these payment types has grown rapidly due to the 2020 Tokyo Olympics, though the Japanese authorities postponed it.

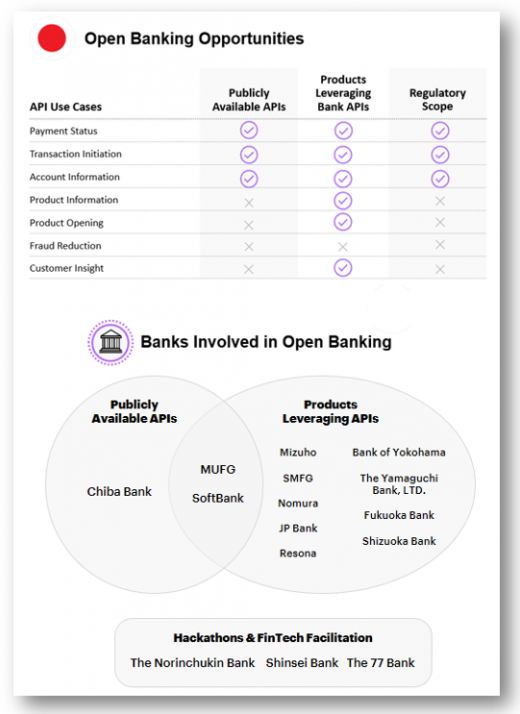

The measures to adopt Open Banking are versatile. Yet, the most common ones are the collaboration between national and regional partners and partnerships between banks without building API portals.

A notable change happened in October 2017, when three megabanks — Mizuho, Sumitomo Mitsui, and MUFG — agreed on establishing a universal QR payment system. Another milestone was reached in May 2018, when Resona Banks, Fukuoka, and Yokohama collaborated to build a QR code payment system called “Yoka Pay.”

Despite the scope of initiatives, many Japanese banks decided to team up once they become compliant with the new regulations.

What’s Next for Open Banking Worldwide?

When Open Banking became mature in the U.K. and Japan, financial players readily adopted the system. Meanwhile, Australia is yet to go through this process.

In all the reviewed countries, the government initially led Open Banking initiatives. In the future, local banks and authorities will continue carrying out related initiatives to ensure Open Banking’s sustainable development worldwide.

The post The Many Faces of Open Banking: Australia, the U.K., and Japan appeared first on ReadWrite.

(15)