Tilt Wants To Be Venmo, But Everywhere

James Beshara, CEO of the crowdfunding platform Tilt, has long resisted turning his app into a vehicle for sending one-on-one payments. “We never found [peer-to-peer] that interesting,” he says.

But Beshara says his users, particularly those overseas, kept demanding it. So, despite his reservations, the company is launching “pay” and “request” buttons that will allow users to pay one another without running a crowdfunding campaign. The new features mimic those already available on Venmo, a peer-to-peer payment app built around an emoji-filled social feed popular with millennials..

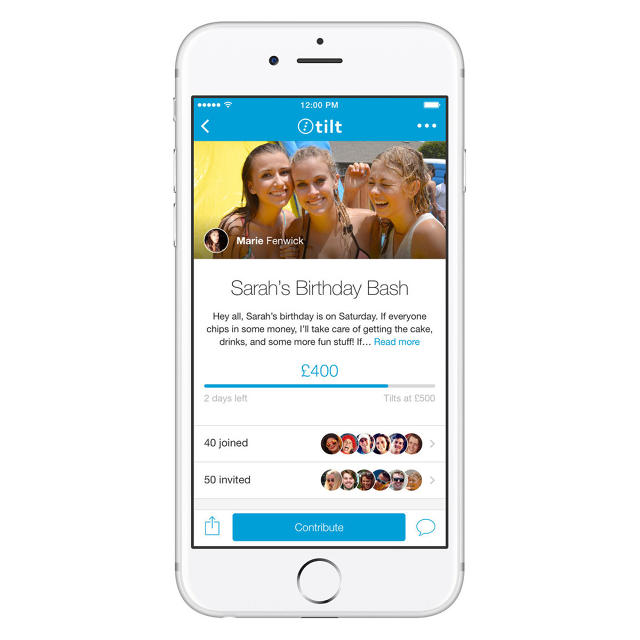

Tilt is a mobile app that allows a person to crowdfund a project from a specific group of people, whether a club or a group of friends. The platform doesn’t have rules around what a person can pool money for, but if they’re selling a product, Tilt will apply a 2.5% fee to the total amount raised. The app is designed for social scenarios, like collecting money from a group of friends for a weekend trip or perhaps running a fundraiser for a cause among a more intimate group of people, and has gained interest among college students. Roughly two-thirds of Tilt users are between 18 and 24, says Beshara. But jumping into direct payments between individuals pits it up against Venmo.

Venmo, which is a subsidiary of PayPal and processed $3.92 billion in the second quarter alone, is a big fish to fry. Yet, while the app has grown rapidly in the U.S., it has yet to launch in other countries. This could give smaller players, like Tilt, a chance to scoop up a global audience before Venmo finally makes its way overseas (if it ever does).

“There’s kind of this feeling of [Venmo] not really innovating,” says Beshara. “But even more than that, it’s a seven-year-old product and still only in one country.”

PayPal acquired Venmo by way of Braintree in 2013. The payments company has done precious little to update Venmo in years since. But now, after three years, PayPal is slowly rolling out the ability to pay with Venmo at select retailers. Still, the app remains confined to the U.S. PayPal hasn’t been explicit about why it hasn’t launched the app in other nations, but here are a few reasons why Venmo remains a U.S.-only property.

One, the company may be acting overly cautious, because they have a hot commodity on their hands. They might not want to change it for fear of losing the loyal following the app has already amassed. Two, PayPal may be concerned about brand confusion. PayPal and Venmo do exactly the same thing. They allow people to hand off money to one another digitally. This has forced PayPal to compete with itself in the U.S. and it is probably loathe to cannibalize itself overseas. Three, Venmo isn’t making PayPal any money, because transactions are free. If it does ever push Venmo across the pond, it will likely be after PayPal figures out how to monetize it. While, the company probably would have liked to shutter Venmo and folded it into PayPal, the reality is that if PayPal killed off Venmo, there’s no guarantee that its users would move over to PayPal.

Though PayPal has done a lot of work to make its web-originated product mobile-ready, it’s still not a 2016 product. Venmo is made by and for millennials. It’s is not only easy to use, but its social feed is pithy in a digitally savvy sort of way. PayPal is right to be wary of changing the app too much, but waiting too long to grow the product could put a serious dent in Venmo’s potential.

Because someone else will create the new Venmo and roll it out globally. That someone else, right now at least, might just be Tilt. Already the company has launched in the U.S., U.K., Canada, and Australia. Furthermore, it has many of the features that make Venmo sticky. Like Venmo, it features a social feed, but rather than just surfacing transactions, it also lists fundraisers. In addition to emojis, users can also drop gifs into their comments.

With $62 million in funding accrued from well-established firms like Andreessen Horowitz, Tilt may be poised to establish itself as the social payment app for a global audience.

There’s just one problem with becoming the next Venmo: profitability. As mentioned earlier, Venmo doesn’t make money. Peer-to-peer payments “won’t be a revenue generator,” acknowledges Beshara. Direct payments made with a debit card will be free, but Beshara is hoping that peer-to-peer payments will indirectly spur more Tilts that do generate money for the company.

It’s not guaranteed that users pulled in by Tilt’s peer-to-peer offering will want to crowdfund, and Tilt could find itself losing a lot of money on peer-to-peer. However, it could be a worthwhile risk if Tilt is able to gain traction overseas ahead of any plans by Venmo to launch internationally. Remember, it was teeny tiny Venmo that once posed a threat to big bulky PayPal.

Fast Company , Read Full Story

(107)