What’s Next For Illumina?

For a while, Illumina—the 800-pound gorilla of genomics—could do no wrong. The DNA-sequencing company’s market cap more than quadrupled from 2012, to peak at a whopping $34 billion, fueled in part by the growing hype around the potential of genomics to transform how we prevent, diagnose, and treat disease, as well as facilitate medical research discoveries.

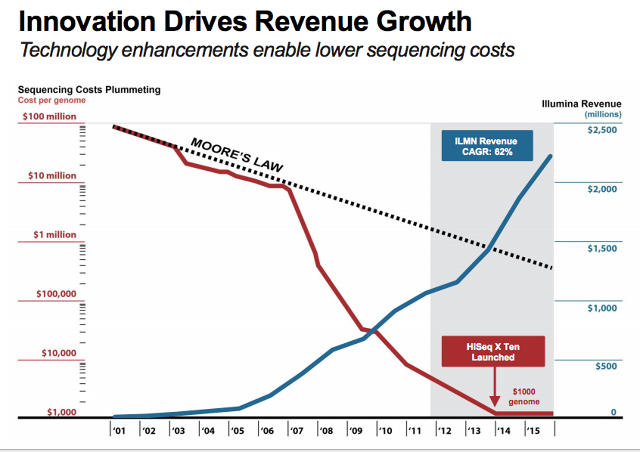

Illumina is also the primary game in town when it comes to DNA-sequencing machines. It has a near-monopoly in the research market, where its instruments have sequenced an estimated 90% of all the human genomes ever sequenced. The company has also been widely credited with being a key player in driving down the cost of sequencing from $100 million in 2001 to a few thousand dollars today (although it’s worth noting that price has plateaued in the past few years).

But in the past three out of four quarters, the company has consistently missed analysts’ expectations in one way or another. Last week, after it announced revenues short of its own guidance, the San Diego-based company’s stock tumbled as much as 25%. That represented its biggest decline in a single day in five years.

What is going on at Illumina, the biotech golden child? Speculation has been rife among analysts. One of the most obvious explanations, put forward last week by Bloomberg, is that the company simply isn’t selling enough of its sequencing machines to justify its insanely high valuation. Illumina’s instruments for analyzing human DNA range in price from $49,000 to up to $10 million. Revenue from its sequencing instruments declined 26% year-over-year, the company revealed in its recent earnings report.

The problem seems to be at the highest end of the market. Foundation Medicine, which is one of an elite group of organizations that have invested in dozens of Illumina’s most expensive and highest-throughput machines—the HiSeq 2500 and 4000—has spent years building out its team of bio-informatics experts, scientists, and technicians. Sequencing is not as simple as taking a sample, plugging in the instrument, and waiting until the data spits out.

“Sequencing is difficult to perform at scale with high accuracy,” explains Foundation Machine CEO Michael Pellini, whose company focuses on patients with cancer. “That’s why there are only a handful of centers doing comprehensive genomic profiling, or whole genome and exome sequencing.”

As Leslie Biesecker from the National Human Genome Research Institute recently told me, the number of people who have been sequenced in the United States is probably in the “five digit” range, which is still a sliver of the population (note: 23andMe, which has more than a million users, offers genotyping services, which is technically different than sequencing). Illumina’s most expensive machine—the HiSeq X Ten—is capable of sequencing 18,000 human genomes each year. That’s a lot of capacity, given the demand for sequencing.

Moreover, the well-funded labs that have invested in these machines will use them for their own research purposes, but they are also actively courting third parties (smaller labs and companies) to manage their samples, too. That eats into sales of Illumina’s cheaper and smaller machines, as well as the consumables it sells. As Bryan Brokmeier, director and senior equity analyst at Cantor Fitzgerald, put it in an interview with CNBC, “Illumina has cannibalized themselves.”

To be fair, Illumina’s executives seem well aware of that. Its executive leadership, led by new CEO Francis DeSouza, has been making the rounds at industry conferences to tout the enormous potential of other markets—namely clinical and consumer. Most industry experts agree that the clinical sector is an order of magnitude larger than the research market, but it’s not easy to jump from one into the other. The clinical market is highly regulated and the customer needs are fundamentally different.

Experts I spoke to say that Illumina would also need to fundamentally rethink its business model to sell into the clinical market. Clinical labs don’t buy expensive equipment and re-agents—the consumables—in the same manner as a large research institution. Oftentimes, the machines will be available for next to nothing, and the companies will enter into a rental agreement for the re-agents. “It will require a very meaningful shift in pricing,” says Pellini.

Illumina might also have a harder time getting paid, which Pellini describes as “very challenging” given the complexities of the insurance industry. “We have an army of people working through reimbursement issues,” he adds.

Illumina dominates in its core market—research—but it is far from the only player jostling to bring sequencing technology into clinical labs. There’s up-and-comers like Oxford Nanopore to contend with, as well as giants like Roche. Illumina “will be competing with multiple well-financed entities with large market caps,” says Mark Blumling, chief executive officer of consumer genomics startup Genos, which is a potential competitor to Illumina spinout company Helix. And it will take time to make a dent, says Blumling: “The clinical market hasn’t take off as fast as the market anticipated.”

In Search of Killer Apps

Many are wondering whether Illumina’s future depends on it building the next killer clinical app. But on that quest, Illumina will inevitably walk a fine line in how it appears to compete with its customers. In the past decade, it has seen some promising new clinical markets open up, including non-invasive pregnancy screenings for genetic disorders like Down syndrome ($2.4 billion by the end of 2022); and so-called “liquid biopsy” tests to monitor late-stage cancers (an estimated $1 billion market by 2020). The consumer genomics market is also showing strong potential, with companies like 23andMe and AncestryDNA now boasting a million users apiece.

Will Illumina make its money as a supplier to these companies? Or will it spin out its own applications? “I think entrepreneurs, investors, and companies are at times apprehensive about Illumina and worried about if, and when, they might choose to compete against them,” John Stuelpnagel, Illumina’s cofounder and former chief operating officer, told me recently. Those concerns seemed justified in 2013 when Illumina bought Verinata Health, a competitor to one of its largest customers, Natera. Both companies offer pre-natal testing services.

All eyes are now on Illumina’s “moonshots”: Its forays into consumer genomics with Helix (an app store for genomics) and Grail (a screening test for cancer). If either of these companies take off, it might be worth it to rustle a few of its customers’ feathers. But until then, some analysts say it’ll need to prove to the market that its sky-high valuation is justified.

Fast Company , Read Full Story

(18)