Who’s Backing The Chain Gang?

Who’s Backing The Chain Gang?

by

Joe Mandese @mp_joemandese, (February 20, 2018)

It’s been nearly a year since I published my first

story about blockchain technology being offered as a solution for Madison Avenue’s media-trading woes, and the marketplace has turned into quite a, well, chain gang. We’ve published about 100 stories about blockchain since then — and, judging by the rest of the trade and consumer press, it’s on the cusp of being this year’s “Big Data,” “programmatic,” or “transparency” in terms of industry buzzwords that people sort of understand, but fundamentally end up scratching their head about.

I’m not willing to bet any crypto — yet — that “blockchain” will rank as the Association of National Advertisers’ “Marketing Word of the Year,” but I have to believe it is a contender based on the reaction to

Unilever’s disclosure at the Interactive Advertising Bureau conference last week, that it’s working with IBM to deploy a blockchain that will create a more secure trading infrastructure for its nearly $10 billion a year in marketing spending.

I first learned about blockchain from my friends on Wall Street, including one who specializes in high-speed trading systems analogous to Madison Avenue’s programmatic media-buying markets. I recall him gushing about how blockchain will transform all transactions — not just Wall Street’s or Madison Avenue’s trades — but everything from buying a house to licensing and paying royalties for music rights. He then handed me a white paper that was three fingers thick. I’ll be honest. I’m still going through it.

One of the first salient pieces I read on how blockchain could impact Madison Avenue, was Media Insider and Simulmedia Founder

Dave Morgan’s 2016 piece. In it, Dave speculated how blockchain could disrupt the supply and demand of the underlying asset Madison Avenue trades: people’s attention. And, a year and a half later, that indeed appears to be how some players are developing it, most notably, Brendan Eich’s “Basic Attention Token,” or BAT.

Eich, a Silicon Valley pioneer who was a founder of Mozilla, and was infamously forced out as its chief, created an even more state-of-the-art browser called

Brave that picks up where Mozilla’s Firefox left off, giving users even more control over what they see and what they do not when browsing computer or mobile screens. But what really differentiates Eich’s model is BAT, which seeks to tokenize the attention users pay to publishers’ pages when they browse via Brave, using that attention as form of currency trading with advertisers and agencies and paying publishers for their content.

The security of its underlying blockchain technology aside, BAT’s model is an ingenious solution to the kind of micropayment system the digital publishing industry has been seeking to deploy for decades: a simple, frictionless method for consumers to pay their favorite publishers for consuming their content.

The biggest problem with Eich’s model is that it insinuates his platform as the new gatekeeper interchanging — and importantly, determining the value exchanged between the stakeholders. I don’t know exactly what his splits are today, but when he first explained the concept to me, it was going to be a third of the value to the publisher, a third to Brave, 15% to overhead, and 15% to the consumer.

But even that last share was confusing; Eich couldn’t explain exactly how the consumer would reap that value. Based on his more recent descriptions, it seems like BAT has evolved into a token for consumers to unlock access to media content, not a means for them to actually get paid for their attention. And that is very much in keeping with Madison Avenue’s historic “borrowed interest” model for advertising and media buying, so I can see how it has evolved that way.

The other big downside to BAT is that it — so far — is dependent on utilizing Brave’s browser, which means it is browser-dependent, at least for the foreseeable future.

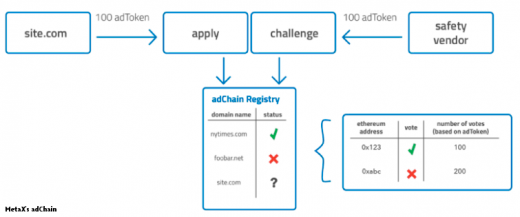

Other notable blockchain solutions tokenizing advertising’s “attention economy” include MetaX’s

adChain and Ternio’s “blockchain for digital advertising.” From what I can tell, adChain is leveraging its technology to effectively gate-keep publisher inventory into a more secure and transparent form of a classic ad network, while Ternio is powering a neutral solution to provide any stakeholder in the mix with a blockchain-based open, transparent and distributed ledger.

My greatest concern with all of these models is their concurrent agenda to mint new currencies they claim are necessary to tokenize media and advertising trading, especially their ICOs, or initial coin offerings. Like a stock market IPO — or initial public offering — ICOs raise capital from speculative investors who believe the coins being minted by these offerings will grow over time.

The most famous — or infamous, depending on your view — is Bitcoin, which is the poster child for cryptocurrencies powered by blockchain. While Bitcoin is best known, Ethereum’s Ether is the most popular, and most open source, for developers, and many of the Madison Avenue solutions either develop on Ethereum’s so-called “smart contract,” or they utilize open source versions of it.

The smart contract is ingenious and would seem to be a logical solution for the ad industry’s transparency issues, because it ensures that every party of a contract gets to see exactly what the state of the contract’s fulfillment is at every stage of the contractual process. When the terms of the contract are fulfilled, the payment is made instantaneously utilizing some form of cryptocurrency as the method. The upside is that there is zero “float” and zero risk to suppliers participating in an advertising contract. And there is zero risk that advertisers will pay for something other than what they contracted for. Of course, the devil will be in the details of the contract itself, and even if it’s a smart one, it has to be structured in a way that explicitly delivers what each participant expects. But when that happens, it’s 100% transparency, instantaneous and frictionless.

What I still don’t understand is why these solutions need to be funded by millions — possible much more — in ICOs, and why, over time, the coin markets associated with these solutions won’t become as, or even more valuable than the advertising markets they were conceived to improve.

It feels like a gold rush powered by the frenzy of Bitcoin and other crypto markets, coupled with the fact that the ad industry actually needs something like blockchain to take friction out of its process.

When I spoke to team at Ternio recently, they said their ICO is fundamental to creating an intrinsic, independent value system that could be utilized as a proxy for trading Madison Avenue’s extrinsic values. What they didn’t explain to me, is why they needed to raise millions to do that.

According to the real-time ticker on Ternio.io’s homepage, the company already has raised nearly $2.5 million in pre-sales of coins in its ICO, which is slated for April 2. (Good thing they didn’t schedule it a day earlier, but the adjacency is nonetheless ironic, if you ask me.)

When I pressed them, they said the funds are also necessary for Ternio to build its technology and, importantly, to reward “miners” who enable the nodes that will be necessary for processing thousands, or potentially hundreds of thousands of advertising transactions in real-time. Without going into technical detail, blockchains require the resources of users known as miners who help process the transactions as part of a distributed network infrastructure. It is actually part of what makes blockchains so secure. If you want to geek out more on it, there’s a great New York Times story explaining it

here.

What I didn’t understand from my conversations with Ternio Co-Founder Ian Kane is why they need to fund their model via an ICO versus conventional methods like venture capital, etc.? And what the implications of seeding and concurrent currency marketplace has for Madison Avenue?

As I was contemplating this column wrapping up my most recent thoughts about blockchain, Brian Wong posted an interesting

article on LinkedIn over the weekend, including his thoughts on the value of yet another potential ICO. Wong is the founder and CEO of Kiip, which to date is one of the purest play examples of an actual attention economy on Madison Avenue. Like Joe Marchese’s and David Levy’s True[x], Kiip was premised on creating rewards for consumers who fulfill trades with brands bidding for their attention.

While the back-end of that process is obscure to most consumers exposed to Kiip or True[x] campaigns, the end result is the same: making an explicit offer to a consumer to engage with a brand. Utilizing blockchain and tokenizing those exchanges therefore makes some sense, so I asked Brian the same question I’ve been asking the other blockchain advertising developers: why he would need an ICO to fund it?

His answer was incredibly candid and, well, transparent: “I don’t know.”

“What’s happening is that the industry has become slightly convoluted in terms of all these ICOs that are really just shells for raising money,” he conceded.

And even though he’s already developed the concept of a “kiipcoin,” and the underlying blockchain technology to trade it, Wong says he’s not sure he’ll go the ICO route.

“The token is very real, and it will be rolled out,” he explains, adding that others are using ICOs as a rationale for developing a token.

“In our case, the token already exists,” he says. “It’s not conceptual. It’s based on a private blockchain we created to record the ad transaction details from purchase to view — end-to-end — and the token is simply the representation of the value that is being presented from end-to-end in that funnel.”

Brian concedes that the kiipcoin is still in “beta,” and he’s not yet sure how it will roll out or be deployed, but he says he is very much committed to the blockchain technology that underlies it.

“For us, the main goal is to show that it’s possible to use blockchain to execute and fulfill a media buy,” he explains adding that there is a secondary, potentially even more intriguing aspect to utilizing kiipcoins as a token for media trading. That aspect isn’t for the ad industry or the publishers — in the case of Kiip the thousands of app partners that power its consumer marketplace — but the consumers themselves.

“It could be an important way for consumers to keep track of their value in this chain as well,” he says, envisioning a model in which consumers accrue kiipcoins as a means of managing the value they contribute to the advertising ecosystem.

What do you think about that?

MediaPost.com: Search Marketing Daily

(52)